Table of Contents

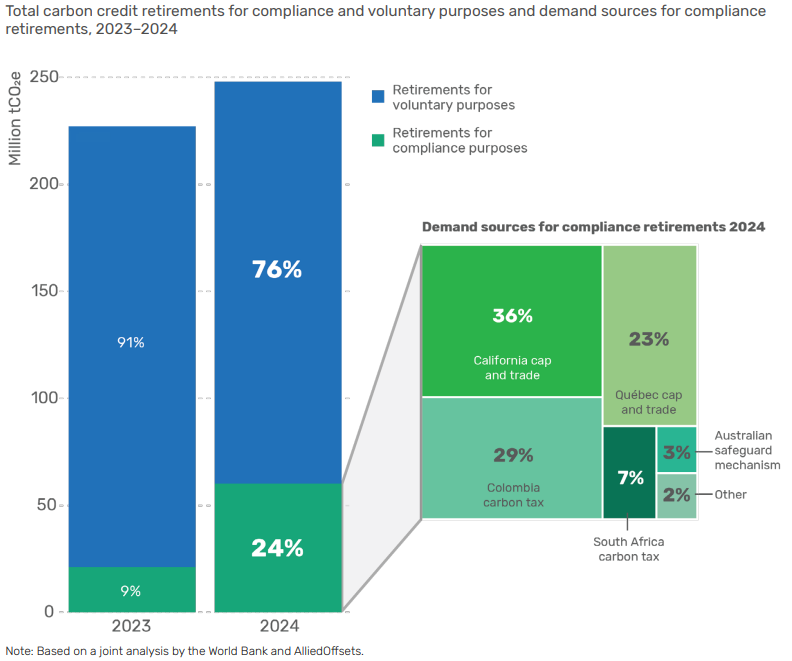

As we already discussed the basics of carbon market in our previous article, now let’s deep dive into the complexity of compliance and voluntary market for the business. For businesses, the carbon landscape is divided into two distinct but increasingly overlapping worlds, Compliance market and voluntary market of emission reduction. As per the study of World Bank 76% retirement has been done for voluntary purposes while 24% has been for compliance purposes. However, the growth in compliance market has been around three fold in just one year.

What is compliance carbon market for the business?

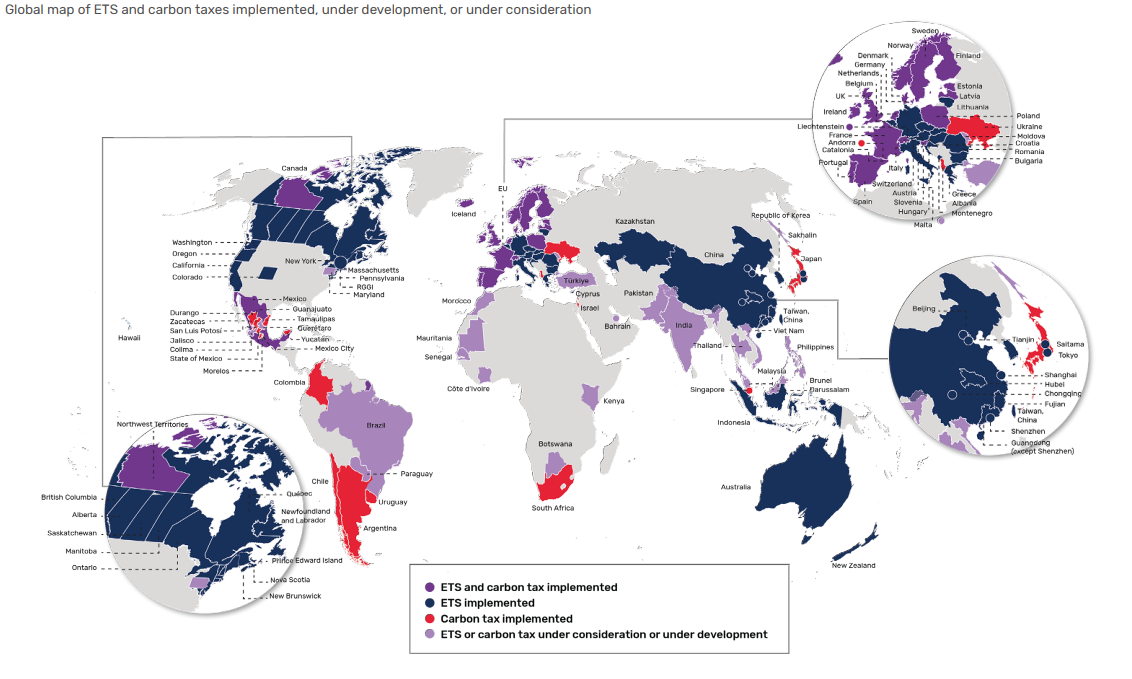

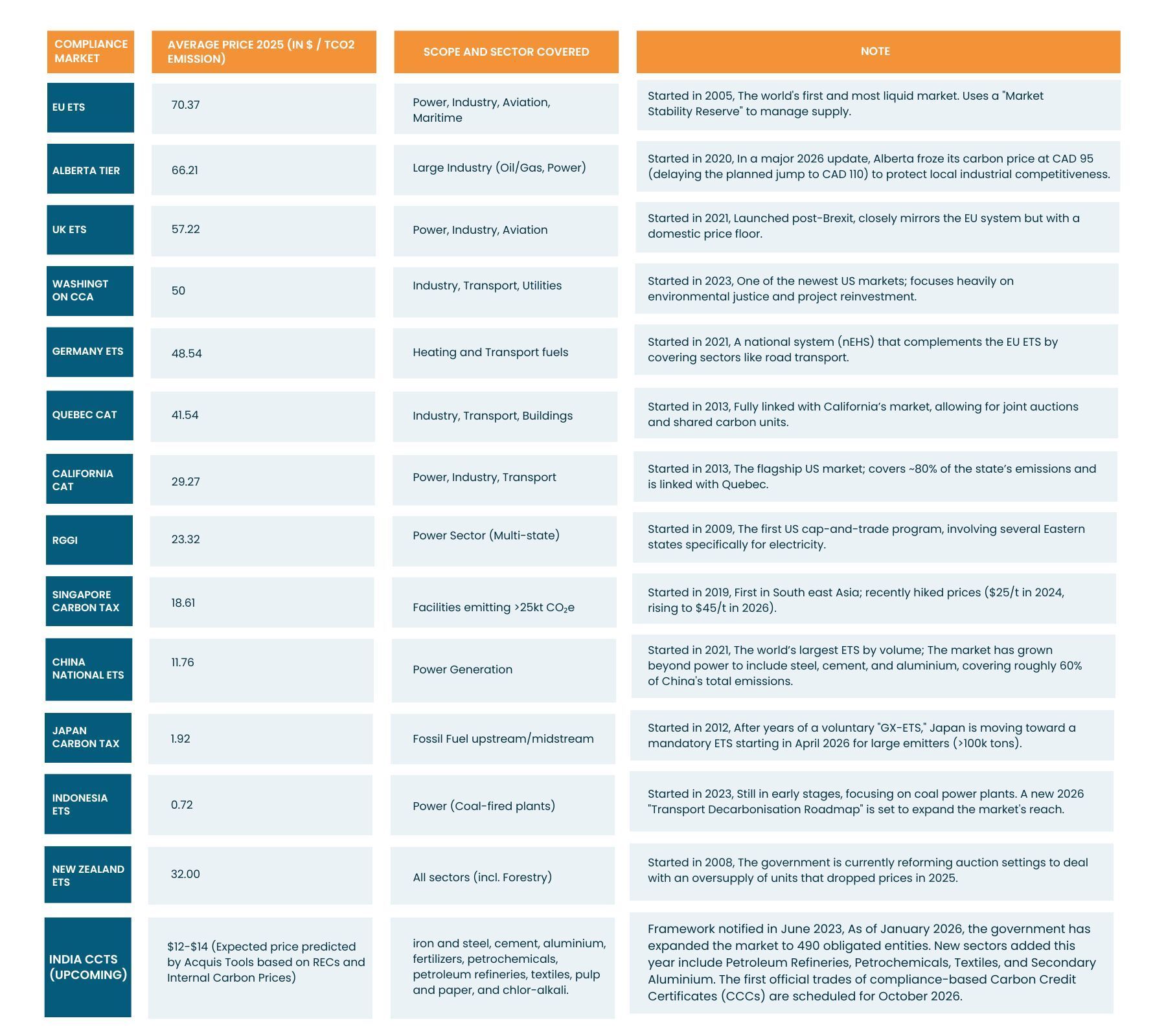

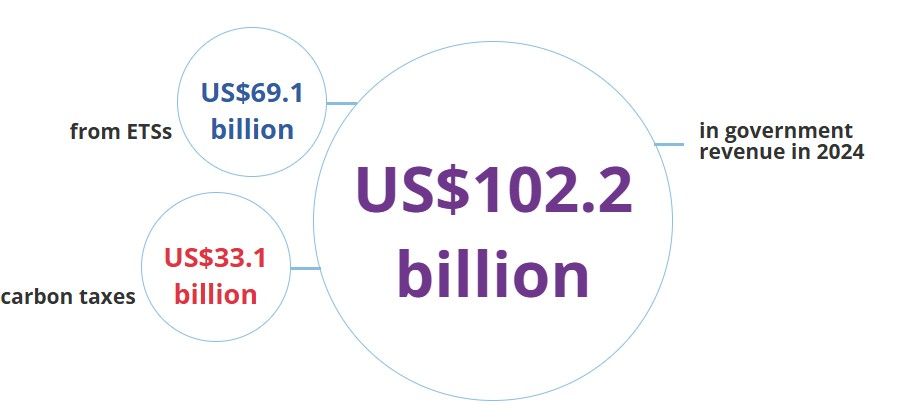

These are mandatory markets created by government regulation (e.g., EU ETS, UK ETS, USA Regional market, India’s upcoming CCTS). Participation is a legal obligation for covered sectors. The price of carbon here is driven by regulatory stringency. Carbon pricing now covers around 28% of global GHG emissions, with 43 carbon taxes and 37 ETSs in place. Jurisdictions comprising almost two-thirds of global GDP have a direct carbon price in place and the largest middle-income economies, including Brazil, China, India, Indonesia, and Türkiye have implemented or are moving toward implementing carbon pricing. Despite a slight reduction in carbon pricing revenues, globally ETSs and carbon taxes continued to generate over USD 100 billion.

Compliance market are designed for the high emission sectors like power sector, cement, steel, aluminium, aviation sectors and many heavy industries. These entities must follow the compliance and adhere to government set emission threshold. Nation with compliance market has regulatory bodies to set the limit and allow the auctions for extra allowance.

In 2025, companies like Clean Energy Fuels Corp. (CLNE), Darling Ingredients, and NextEra Energy are leveraging carbon compliance markets not just for regulatory adherence, but as a core profit centre. Their business model hinges on producing energy or fuels with carbon intensities significantly below the statutory "caps" set by programs like California's LCFS or the federal RFS. By doing so, they generate surplus compliance credits effectively a high margin, floating-rate asset, that they sell to "obligated parties" (such as traditional oil refiners or utilities) who cannot meet their own emission targets.

Tesla remains the primary case study for monetizing compliance. Because Tesla sells only zero-emission vehicles, it has no compliance obligation and sells its excess Zero-Emission Vehicle (ZEV) credits to legacy automakers with high-emissions fleets. In Q1 2025, Tesla reported $595 million in regulatory credit revenue.

What is voluntary carbon markets (VCMs) for the business?

Many corporations voluntarily purchase carbon credits to fulfil internal climate targets or meet consumer expectations. While these purchases aren't legally mandated, they allow businesses to claim "carbon neutrality" and demonstrate their commitment to corporate social responsibility (CSR) and brand values. When a company cannot meet its greenhouse gas (GHG) emission targets directly, it can buy offset credits. These credits fund environmental projects designed to avoid, reduce, or remove carbon from the atmosphere. However, the market faces significant scrutiny over credit quality, leading to frequent concerns about "greenwashing."

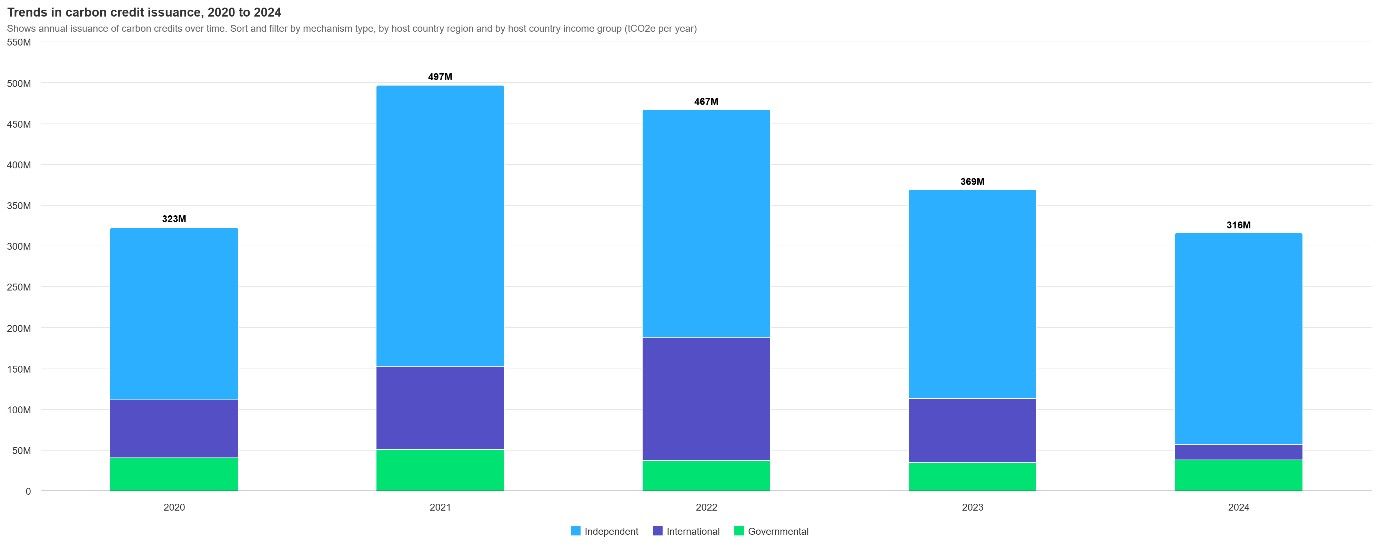

(Note: Carbon crediting mechanisms are classified according to the type of organization that administers them: International: Includes mechanisms established under international treaties and administered by international organizations. Independent: Includes standards and crediting mechanisms administered by independent, non-governmental entities. Governmental: Includes mechanisms administered by one or several regional, national, or subnational governments.)

More than 300 million carbon credits generated during 2024, in which 260 million are coming from independent entities which registered their projects at different registries. There are different types of projects such as reforestation, renewable energy, community based program, nature based solutions etc., these projects generate carbon credits that further buy and sell through different registries. These credits are verified by different independent accredited third party verification bodies like Verra, Gold standard, Climate action reserve, American carbon registry. And from demand perspective, VCMs has dominated by private companies to fulfil their internal commitments such as RE100 and CDP program.

Voluntary market shift has moved significantly toward high-quality carbon removals (physically pulling CO2 out of the air) rather than just "avoided emissions" (paying someone else not to pollute). This shift has moved the market away from simple "avoidance" credits toward high-integrity "removals," where companies like Microsoft and Stripe provide the upfront capital for advanced solutions like Direct Air Capture (DAC) and ocean alkalinity enhancement. These investments not only help businesses achieve their "Net Zero" claims but also accelerate the commercial viability of green technologies. In practice, 2025 has seen major industry players integrate carbon credits into their core business models to drive tangible environmental and social change.

While on the other side, In 2023 we have seen that Apple launched its carbon neutral watch and later got sued by consumers in California for false promise. While apple has done the voluntary retirement of RECs (renewable energy certificates), and voluntary offsets credits for scope 2 and 3 respectively. It is interesting to look into the Cost of offsetting the carbon neutral product which Apple claimed in its launch. As per their own data and some calculation, it cost less than a $1 to offset the emission caused by the product (carbon neutral Apple watch) which is priced at $799. Offset cost to product price ratio is 0.12%, This means Apple spending less than 0.12% of the total price to make its product carbon neutral and advertise it as a premium high price product. This could be called as greenwashing marketing rather than environmental concern.

How these markets regulate the business strategies?

In 2026, the landscape for carbon management has shifted from voluntary "goodwill" to a core financial and operational necessity. As regulations like the EU’s Carbon Border Adjustment Mechanism (CBAM) enter their definitive phases, corporations are moving beyond simple offsets and adopting more robust Response Strategies.

Corporations are adopting three primary strategies to navigate this:

Internal Carbon Pricing: Companies are voluntarily setting an internal price on carbon to test the resilience of their investments against future regulations. Rather than waiting for a government tax, companies are "taxing themselves" to future-proof their balance sheets. This involves assigning a theoretical or actual dollar value to every ton of CO2 produced. The goal of this shadow pricing is to ensure that a project that looks profitable today doesn't become a "stranded asset" tomorrow when carbon taxes rise.

Resource Shuffling: An exporter might send its "cleanest" steel (produced using renewable energy) to the EU to avoid heavy CBAM tariffs, while sending "dirty" steel (produced with coal) to regions with no carbon costs, though this is a short-term fix.

Data Transparency: Carbon data has become as important as financial data. "Embedded emissions" are now a prerequisite for trade. Contracts are being renegotiated to include clauses requiring suppliers to provide granular data on "embedded emissions". For example, Microsoft and Apple have moved beyond general Scope 2 and Scope 3 estimates. They now require their primary manufacturers to use specific digital platforms to track real-time energy consumption. In 2025-26, if a supplier cannot provide verified, audit-ready data on the carbon intensity of their components, they risk being delisted from the supply chain entirely.

What is Retirements or Redemptions?

Retirement can be defined as the buying carbon credits/certificates and retire (redeem) their value of per ton of CO2 emission from your scope 1, 2 and 3 emission process. This process makes the business compliant and their emission within the prescribed threshold.

What is one credit or certificate?

In both the compliance and voluntary carbon markets, the standard unit of trade is universally defined as one carbon credit (or certificate) represents the reduction, avoidance, or removal of one metric ton of carbon dioxide (CO2_e) or its equivalent in other greenhouse gases.

What is embedded emissions?

Embedded emissions (also known as embodied emissions) refer to the total amount of greenhouse gases, such as CO2, emitted during the entire life cycle of a product, including the extraction of raw materials, manufacturing, and transportation to the final consumer.

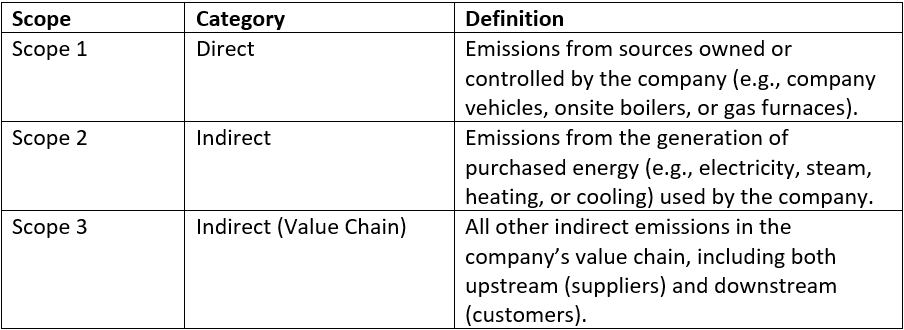

What is Scope 1, 2 and 3 emissions?

Source: All the graphs and data has been used from World Bank portal on status and Trends of carbon pricing 2025.

For a clearer breakdown of how carbon markets function including the mechanics of credits, trading systems, and regulatory structures, Read our detailed guide on Carbon Markets Explained.